September 2024 Space Stock Review

Includes Commentary on: BKSY, RKLB, LUNR, SATS, VSAT, CMTL, and BA

Hello fellow space enthusiasts! 🚀

In this month’s Space Stock Review:

📈 Market Overview

✍️ Space Stock Performance + Valuation

Disclosure/Disclaimer: Case Closed should not be interpreted as investment advice or an investment recommendation; posts represent Case’s personal opinions only. Please do your own research before investing.

1. MARKET COMMENTARY

Public Markets

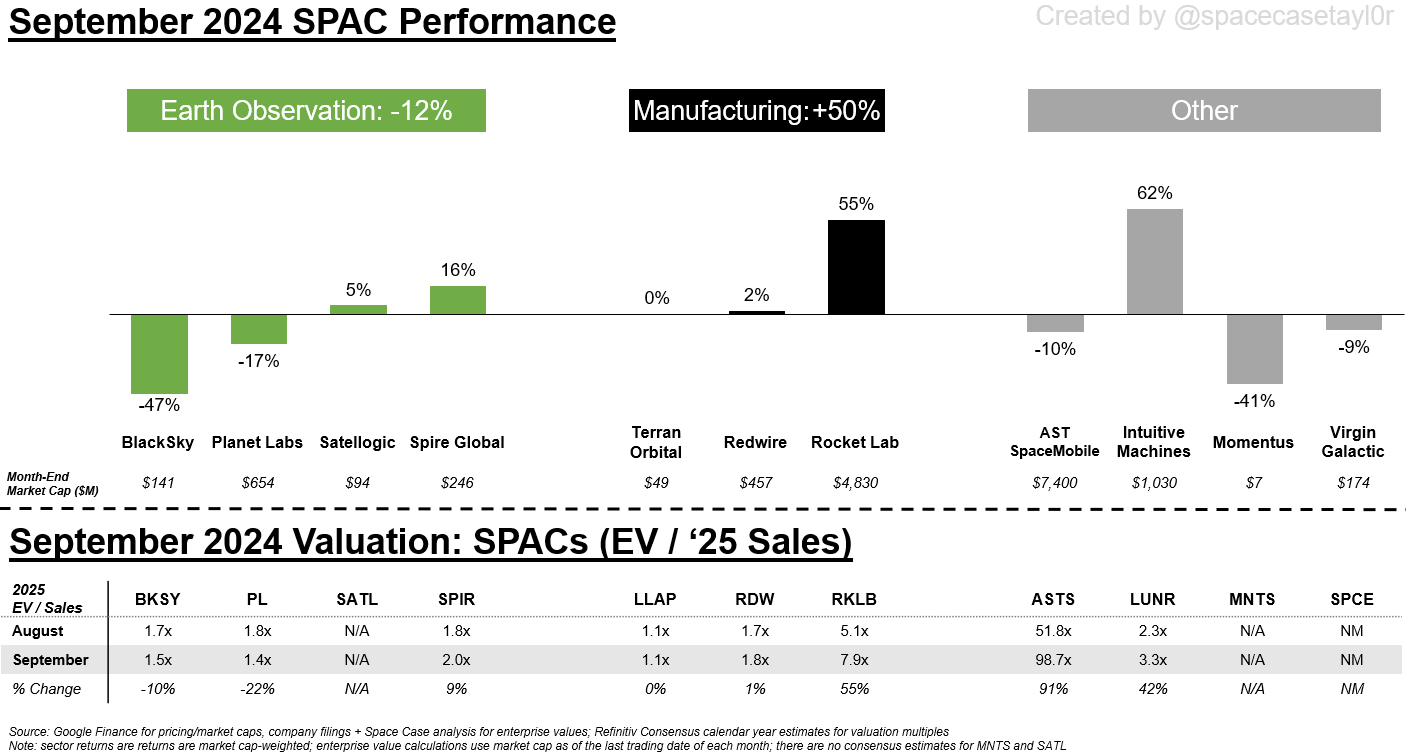

Stocks saw strong returns in September, with the Space SPACs leading the way at +16%.

Investors piled back into stocks in September as the Federal Reserve made its first, long-awaited interest rate cut since beginning a rate hike cycle in March 2022; given a backdrop of continued cooling inflation and other indicators suggesting that the economy is healthy enough to avoid a recession, the positive investor sentiment makes sense.

As I have repeatedly pointed out (link), lower interest rates disproportionately benefit riskier assets, including unprofitable (but higher growth) stocks like the space SPACs, companies included in the ARK Innovation ETF, and tech stocks included in the NASDAQ (link).

While September is historically the worst month of the year for stocks (see below), the S&P 500 actually had its best September performance in 11 years this year (link).

The phenomena where stocks struggle in September is referred to as “the September effect” and while there are many attempted explanations for why this happens most years, my take is that in September, Wall Street is coming back from summer vacation and buckling down to not only finish the current year strong, but begin processing their outlook for the next year; this requires portfolio rebalancing, which results in September stock volatility.

Private Markets

I won’t go into as much private market detail here, but check out these resources for a more comprehensive overview of private market trends:

2. SPACE STOCK COMMENTARY

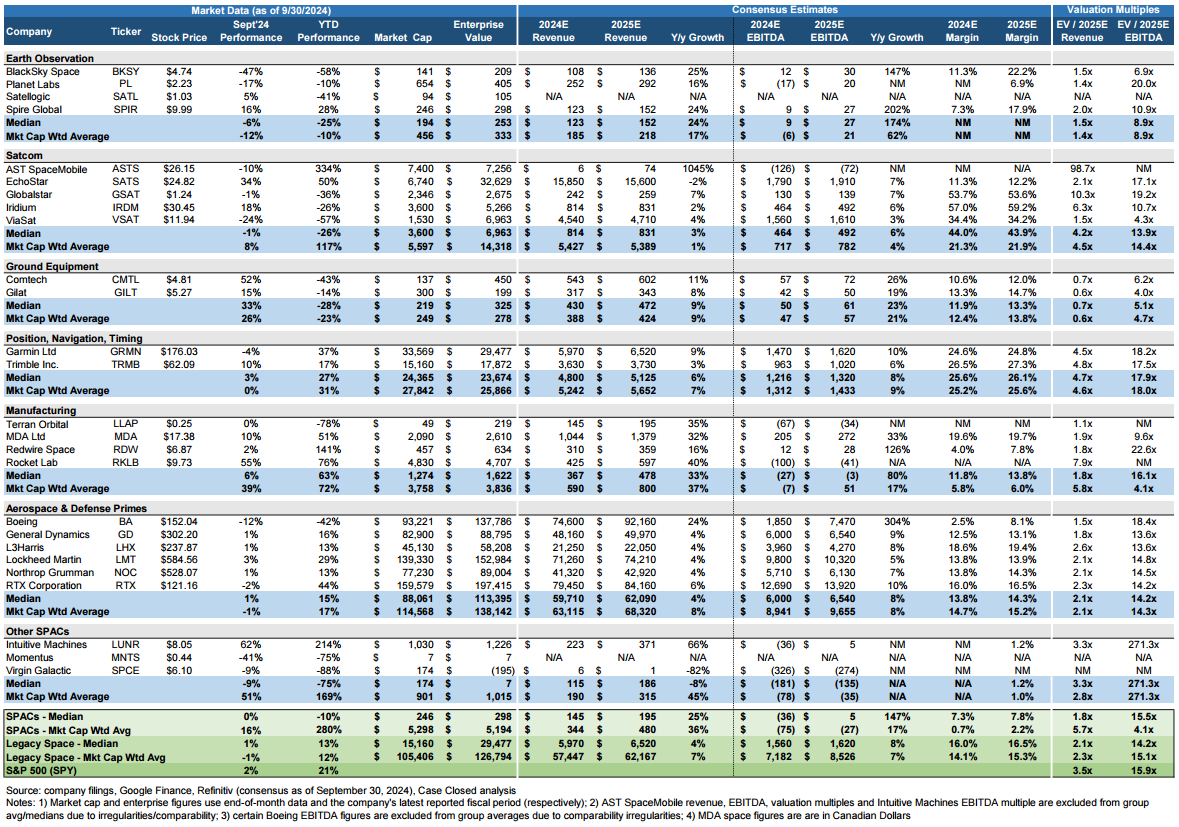

BlackSky / BKSY shares tumbled -47% in September due to the company’s $46M equity fundraise, which diluted existing shareholders by -39%

On 9/4, BKSY surprised shareholders when it announced it would execute a 1-for-8 reverse stock split, meaning that shareholders would get 1 new BKSY share for every 8 BKSY shares they already owned; this would artificially increase price per share while proportionately reducing the number of shares outstanding (and thus keep BlackSky’s equity value unchanged). BKSY shares declined -21% the following day

While management didn’t offer a reason why they were doing this, companies generally pursue reverse stock splits when their stock is consistently trading below the minimum price requirement of the exchange they trade on (ex. trading below $1.00/sh for 30 consecutive days will get you a warning from the NYSE) or else they risk being de-listed (which is bad because it would limit BKSY’s access to investors and and damage its reputation); BKSY shares had been trading at +/- $1.00/sh for the last 12mo, but hadn’t violated NYSE minimum price requirements

The clear readthrough from this action was that management was proactively increasing BKSY’s price per share because they intended to raise capital via an equity raise, which would dilute existing shareholders and drive down BKSY’s share price. If they hadn’t executed the reverse-split, BKSY shares would have almost certainly traded below the minimum $1.00/sh after the raise (they were at $1.11/sh the day before the announcement)

It took another three weeks, but BKSY did formally announced an equity raise on 9/24; it initially planned for a $40M raise (vs a pre-split market cap of $163M) but ultimately raised $46M, a 39% dilution for existing shareholders (based on number of shares outstanding). Unfortunately this raise distracted from the fact that BKSY announced three more contract wins in the month of September with defense, civil, and commercial customers

The reverse share split and equity fundraise/dilution was surprising because one month before the split on the 2Q earnings call in August, management had said they believed they had “sufficient liquidity for the foreseeable future” with cash on hand + anticipated customer payments + vendor financing. However, it seems that management needed to raise additional cash “to gain more control over the parties that impact our Gen-3 supply chain and production operations” (per ‘use of proceeds’ commentary in the company’s prospectus, link)

For context, BKSY is averaging mid to high-teens cash burn on a trailing 12mo basis, but investments related to the company’s Gen-3 satellites are driving heightened capex over the next 18mo

Rocket Lab / RKLB shares launched upwards +55% in September, propelled by general market sentiment

I don’t think there was any one catalyst that drove Rocket Lab’s strong performance in September; instead, RKLB benefitted as investor enthusiasm for taking on more risky assets grew throughout the month—evidence of this can be seen in RKLB shares beginning a +67% run from 9/6 through 9/30, which matches the same timeframe where the S&P 500 / SPY reversed a local minimum and began a similar (but smaller in magnitude) movement upwards through the end of the month

I am biased, but I view RKLB as the highest quality space SPAC in terms of management and execution + many investors view the company as the closest thing to SpaceX they can own in the public markets, so it makes sense to me that the company has benefitted as near-term market sentiment towards unprofitable / growth stocks has improved

However, the most recent move puts RKLB at a rich valuation—its $5.5B enterprise value (as of 10/16/2024) is the highest the company has been valued at in 35mo and its 11.2x next 12mo revenue multiple is its highest in 29mo. Investors who are planning to hold onto RKLB shares longer term would probably note the company is much cheaper if you look at its 2030 revenue multiple (currently 2.2x based on Koyfin consensus estimates as of 10/16)

All this is to say—know what you are underwriting if you are investing in the stock at these levels

Intuitive Machines / LUNR saw a massive +62% movement in September following its contract win for NASA’s Near Space Network (NSN) services, where it will provide communications and navigation services at the moon to support the Artemis lunar exploration campaign

Retail investors online were freaking out when this award was first announced because it has a maximum potential value of $4.8B (yes, billion) which would be quite a win for a company with a market cap of $694M prior to the award announcement

However, this contract is an IDIQ (Indefinite Delivery/Indefinite Quantity), a type of contract used by the U.S. federal government (USG) to purchase goods and services when the USG doesn't know the exact quantity of a product or service it needs, but it does know the general range. IDIQs always have a giant maximum value, but sometimes there is $0 guaranteed dollars; you can’t count your IDIQ eggs before they hatch

For this NSN contract, Intuitive Machines is guaranteed $150M over a five-year period (link) and can win up to $585M over the first five years (link); if the company executes well over that first five years, NASA has an option to award them another 5yr contract that could be worth up to $4.2B. So yes, a $150M contract is great for LUNR, but it is not a $4.8B contract (only 12% of total potential contract value is guaranteed)

Initially, I though the market’s reaction to this contract was an overreaction because people who aren’t used to government contracting usually don’t know that an IDIQ will have a big headline figure and little guaranteed money (link to a bunch of people calling me dumb on X)

However, I was actually wrong - the market does have a clue what an IDIQ is. since the announcement, the market has basically taken the guaranteed money ($150M), multiplied it by LUNR’s pre-announcement revenue multiple (2.1x) and added the total ($315M) to LUNR’s market cap ($694M pre-announcement; now $1.0B-$1.1B post-announcement)

While we don’t know the mechanics of this contract, I expect management to address this at conferences and/or on its next earnings call. Examples of questions I would have for LUNR’s management team include: Will LUNR receive all $150M of the guaranteed money in 2024 like the market is assuming, or is the award money given out over a longer period of time based on performance milestones? What is the risk that another company gets added to this IDIQ and LUNR has to compete for money vs having a sole source contract? What would it take for LUNR to win all $585M of the initial contract? What is timing for NASA to make its decision for the optional 2nd five-year period?

EchoStar / SATS increased +34% in September, potentially driven by leaked rumors around the long-awaited merger of DISH TV (owned by EchoStar) with DirecTV (owned by AT&T and TPG)

For years there has been speculation around a merger between DirecTV, the leading satellite TV provider and once the largest pay-TV operator in the US, and DISH Network, the other major US satellite TV provider; given that they have both been hemorrhaging pay-TV subscribers for a decade+ following the advent of streaming services like Netflix and virtual Pay-TV operators like YouTube TV and Hulu Live, there was sound logic behind the idea of merging to form a single, stronger satellite TV operator, as well as realize material cost synergies

Most years I dismissed the “news” of DISH and DirecTV being in merger discussions since we hear this rumor every year and nothing ever happens, but with DISH’s parent company EchoStar due to repay $2B of debt in November and it not having the cash on hand to do so, I paid attention when then rumor mill started on 9/13/24 (link); of note, DISH’s founder and Chairman, Charlie Ergen, is known as a wild deal maker and this seemed exactly like the kind of thing he would do to get EchoStar out of a sticky situation (there is an industry saying “never bet against Charlie Ergen;” link to an article that explains Ergen’s background)

Lo and behold, on 9/30 the two businesses announced plans to merge (link to more details around the deal)

Was SATS’ runup the result of leaked rumors around a potential merger? While potential M&A is usually strictly confidential and disclosure by either company or bankers/lawyers involved could count as insider trading, I’m not sure what else would explain SATS performance in the month other than general anticipation of Ergen swooping in to save the day for EchoStar’s debt situation. At this point, it doesn’t matter, but it’s fun to think about the potential drama

ViaSat / VSAT declined -24% in the month as company’s valuation right-sized following unusual volatility in July and August

As I highlighted last month (link), VSAT experienced some unusually volatile share movement over the summer (including a random +38% single-day movement in early August); however, the stock finally returned to pre-volatility levels by the end of September and has continued to decline even further into October

Comtech / CMTL shares launched upwards +52% in September for no good reason

There was no material news for Comtech in September. Given how small the company is ($450M enterprise value, $137M market cap at month-end) perhaps the stock was just a material beneficiary of improved investor sentiment towards risky assets (the definition of which often includes micro-cap stocks, like CMTL)?

Boeing / BA’s stock declined -12% in September, driven by investor concern related to an ongoing labor union strike against the company

Boeing’s bad news continued in September with its largest labor union (33k members) going on strike (link), halting 737 production and “jeopardiz[ing] our recovery” (per the company’s CFO; link)

The WSJ estimates that the strike could cost Boeing $500M a week (link) and credit ratings agencies have warned that they might downgrade Boeing’s debt if the strike drags on; this would be bad for Boeing and certaintly send shares down further given that the company is reliant on debt to fund its business in the near-term as it looks to get back on track with consistent free cash flow generation following a myriad of 737 jet production issues. Boeing is barely above “junk bond” status right now and a downgrade would materially increase the cost of any debt it would attempt to raise (link to my dated, but still relevant discussion about Boeing’s debt and why it wants to avoid a downgrade)