September 2023 Space Stock Review

Bonus: Commentary on ASTS, LLAP, VSAT, BA, and RTX

Hello fellow space enthusiasts! 🚀🛰️

In this month’s Space Stock Review:

📈 September Market Overview

✍️ Space Stock Performance + Valuation

Disclosure/Disclaimer: Case Closed should not be interpreted as investment advice or an investment recommendation; posts represent Case’s personal opinions only. Please do your own research before investing. Case owns shares of ASTS, PL, RKLB and SPIR at the time of this post (10/10/23).

1. MARKET COMMENTARY

Public Markets

Old habits die hard…

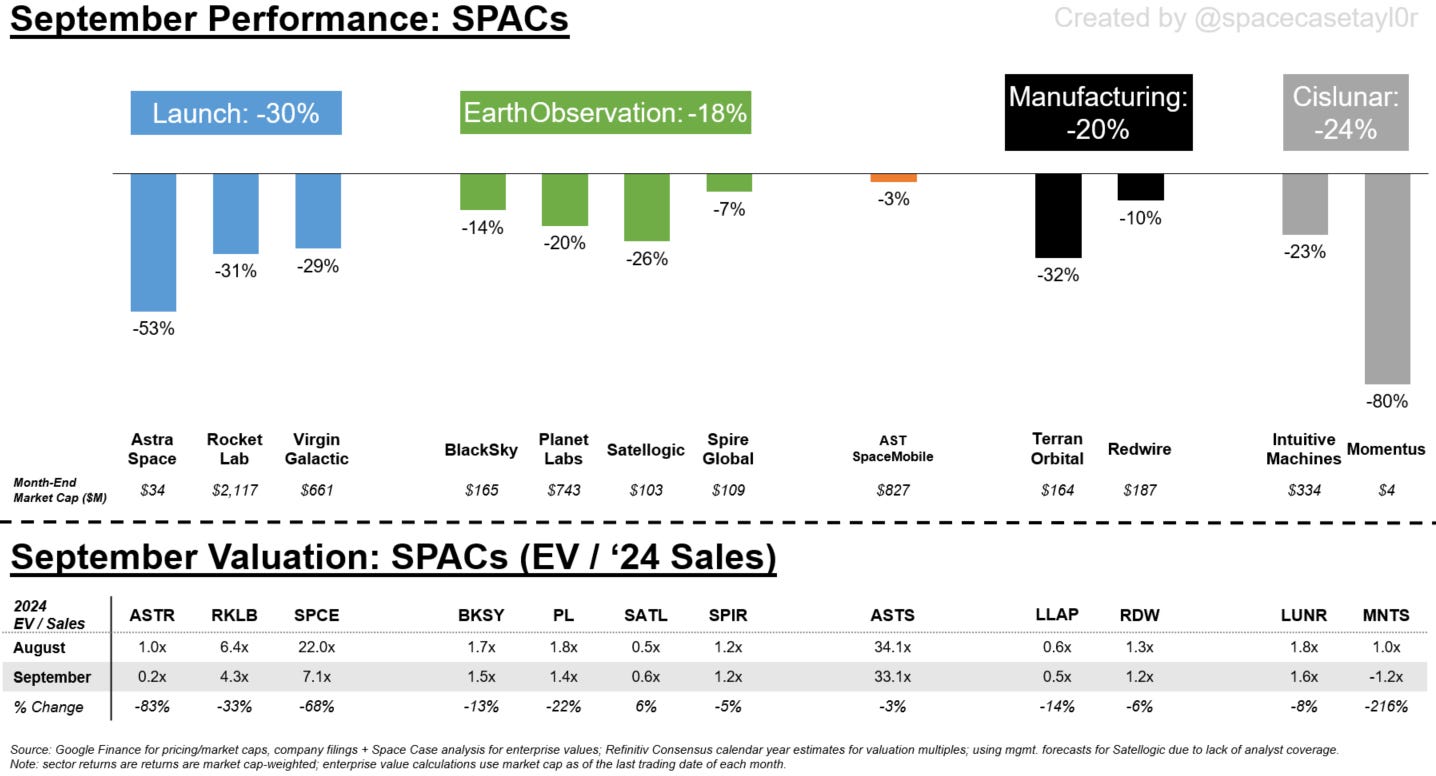

In September the space SPACs registered a second consecutive month of double-digit losses, taking their year-to-date total from +38% at the end of July to -15% at the end of September.

However, it wasn’t just the SPACs that suffered—even the broader market / S&P 500 was down -5% in the month.

These losses are somewhat unsurprising as stocks historically underperform in September, a phenomenon known as the September Effect (see chart below+ link).

There are lots of theories why the September Effect happens each year, but my personal take is that in September Wall Street is coming back from summer vacation and buckling down to not only finish the current year strong, but begin processing their outlook for the next year; this requires portfolio rebalancing, resulting in September stock volatility.

However, this September’s market downturn also has some fundamental drivers—the Federal Reserve indicated that interest rates are likely to remain higher for longer and are not likely to decrease until sometime in 2024; this compares to prior market expectations for potential rate decreases by the end of 2023.

I have no clue how the market is just now digesting the point-of-view of “higher for longer,” I feel like we’ve been talking about “higher for longer” for like a year now (or maybe that’s just been my POV).

Private Markets

I won’t go into as much private market detail here, but check out these resources for a more comprehensive overview of private market trends:

Tech IPOs Could Burn Firms Who Bought Into Hot Startups Too Late

VCs tell start-ups to delay IPO plans after Arm and Instacart underwhelm

Venture fund losses still lag public markets and have yet to recognize the vast majority of losses

2. SPACE STOCK PERFORMANCE + VALUATION

Note: we’ve switched to 2024 valuation multiples—this is typical for analysts and investors to do to at this point in the year, though I doubt most analysts have spent much time refining their 2024 estimates yet and also most publicly traded company management teams probably haven’t given robust guidance / outlook color for 2024 yet. Nonetheless, 2023 is more than half over and Wall Street knows its time to move on.

AST SpaceMobile is finally registering on our multiple comparison at 33x 2024E revenue (the company wasn’t generating revenue in 2023, so it didn’t have a multiple).

While this is a ridiculously high figure (for context, other LEO satcom companies like Globalstar and Iridium trade at ~10x 2024E revenue and AI darling Nvidia “only” trades at 20x forward revenue) that suggests there is downside for ASTS shares, this company has never traded on fundamentals, so I wouldn’t read too much into this figure other than to recognize that investors who own this stock are betting on future prospects (at least) several years beyond 2024.

Terran Orbital is trading <1x 2024 revenue, which likely signifies that investors are skeptical of consensus revenue expectations for $586M of revenue next year.

This skepticism is likely due to uncertainty around LLAP’s biggest customer—Rivada Networks—which awarded LLAP a $2.4B contract to build hundreds of satellites for Rivada’s planned LEO megaconstellation. While a $2.4B contract may sound like good news, Rivada has yet to publicly announce that it has secured funding for its constellation, so the $2.4B contract it awarded to LLAP might end up being fake news if the company can’t secure financing.

3Q/4Q results will be key for LLAP to begin alleviating this uncertainty overhang: management has indicated they expect to receive $180M in payments from Rivada in 2H23 (mostly weighted towards 4Q). If Rivada follows through with these payments, it could signify financial security and begin to help with the uncertainty surrounding LLAP shares (though a bigger catalyst would be actual communication from Rivada that it’s funding is secured).

ViaSat’s string of bad luck over the past few months has the company’s stock trading at levels not seen since 2008.

While the company was supposed to emerge from its merger with Inmarsat in a position of strength, the recent ViaSat-3 and Inmarsat-6 F2 satellite failures instead have the company burdened with debt and facing the prospect of delayed capacity (and monetization) improvements as it regroups.

It will be fascinating to see the insurance process play out for these two satellite failures, as up to $770M in reimbursements are at stake for ViaSat (link).

Price chart as of 10/9/2023

Speaking of companies that can’t catch a break, Boeing had a tough month in September after another widespread 737 Max quality issue that is expected to impact near-term deliveries was discovered (link). We’ve previously written about the company’s 737 woes in our April (link) and March (link) newsletters this year.

RTX (previously known as Raytheon) also struggled in September following disclosure of quality control issues for its PW1100 engine (which powers the Airbus A320 family of planes); the company disclosed this issue is expected to reduce operating profits by $3B-$5B over the next several years (link).