2022 Space Industry Key Themes - Part 4

Commercial Space Stations

This is the 4th of a multi-part series previewing key themes for the space industry in 2022. Check out previous posts below:

Part 1: Geopolitical Competition (see here)

Part 2: Lunar Activity (see here)

Part 3: Next-Gen Rockets (see here)

Post Length: ~1,400 words / 10(!) infographics and pictures

Short-Form Version (aka Twitter Thread): Link here

WHY CARE ABOUT COMMERCIAL SPACE STATIONS?

In late March, four citizens hailing from the US, Canada, and Israel will lead the first private astronaut mission to the International Space Station (ISS).

This will represent the first step of a decade-long process where NASA will transition from operating its own space station to utilizing privately-owned & operated space stations.

Commercial space station development is an underappreciated topic within the space industry—satellite broadband constellations, rocket launchers, and even earth observation companies have gotten much more attention lately due to companies in those verticals going public over the last year or so, as well as a certain public figure that draws attention to his businesses in those verticals.

However, I see two factors that make commercial space stations appealing investments relative to many other new space companies:

Proven Use Cases / Strong Demand

Self-Funded Development

Before we dig into the companies creating new commercial space stations, let’s take a step back to examine why they are even being made.

TRANSITIONING AWAY FROM THE ISS

The ISS is set to retire in 2030, marking the end of an era that began in late 2000 when the 1st humans stayed aboard the station.

While the ISS is a symbol of international scientific collaboration and technological advancement, it is old and expensive:

Build costs were $150 billion

It costs NASA $4 billion/year to operate

Much of its core structures were manufactured in the 1990s

At this point, NASA has set its sights beyond Earth orbit to the Moon and Mars. In order to allocate more of its annual budget to exploring these celestial bodies while still maintaining a presence in low-Earth orbit (LEO) for training, research, and experimentation, the agency has stated its intent to partner with + increasingly rely on the private sector.

NASA’s long-term goal is for commercial space companies to ultimately own and operate their own space stations, with the space agency being just one of many customers.

This new operating model is expected to provide NASA significant cost reductions—over $1 billion/year

NASA also hopes that handing the reigns to the commercial sector will increase overall activity in LEO, as private operators will develop new and innovative use cases to monetize their investment in space infrastructure

Mostly importantly, transitioning space station operation to the private sector will enable NASA to focus on exploring the Moon and Mars

SO WHAT’S THE PLAN, BOSS?

NASA has already begun a two-fold plan for increasing commercial LEO activity:

Award contracts to subsidize the development of commercially owned & operated space stations

Begin enabling private astronaut missions to the ISS

Commercial Space Station Development - Progress to Date

Through January 2022, NASA has awarded >$550M to four different groups for private space station development.

All the proposed plans generally have the same key features:

Ability to house 4-10 astronauts at a time

Modular architecture design to enable use case flexibility and future expansion

Use cases focusing on research, manufacturing, and government astronaut training, but also including tourism, media production, and satellite servicing—with more to develop in the future.

Axiom is clearly NASA’s preferred partner given that it was awarded the 1st commercial space station contract and its station will begin as part of the ISS itself. Axiom’s modules will help increase the usable and habitable volume of the ISS before it separates + operates as an independent space station when the ISS is retired.

Blue Origin’s Orbital Reef is unique in that it plans to utilize parent company Blue Origin, Sierra Space, and Boeing’s space transportation vehicles during construction and deployment, while the other space stations will have to outsource those services.

Nanorack’s Starlab is starting out as a smaller, but more agile space station—only able to house four astronauts, but deployable in a single mission.

Northrop Grumman’s proposed space station is more unknown, and the company is still seeking additional partners.

Private Astronaut Missions to the ISS - Progress to Date

In the meantime, NASA plans to greenlight ~two private astronaut missions per year to the ISS so that future commercial station operators can gain experience with mission planning and operations before setting out on their own.

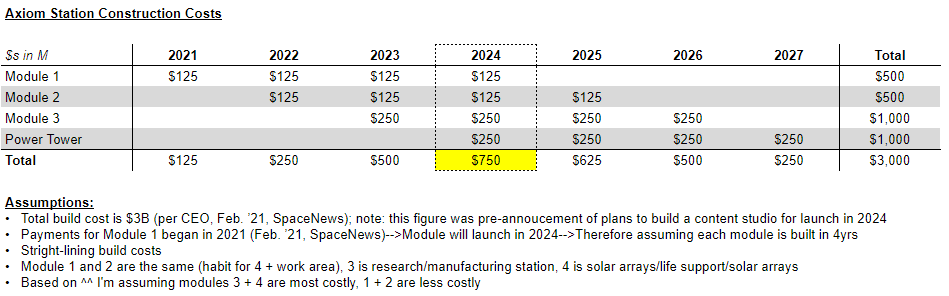

Thus far, NASA has selected Axiom Space to lead the first two of three proposed private missions to the ISS that are planned for 2022 and 2023—the first taking place no earlier than March 31, 2022. The missions will help Axiom Space practice skills + build relationships with necessary partners ahead of when it starts building its own space station in 2024.

TAKING A CLOSER LOOK AT: AXIOM SPACE

Axiom is clearly the overall leading commercial space station developer, given its early support from NASA and its success in securing the 1st two private astronaut missions to the ISS.

After analyzing Axiom’s business development plans, I see two factors that make commercial space stations appealing investments relative to many other new space companies:

Proven Use Cases / Strong Demand: Commercial space stations present obvious use cases that have already been proven out via operations on the ISS. Seemingly, both government and non-government customers are ready to pay up—Axiom’s CEO previously commented that in particular, foreign government demand for use of commercial space stations is very strong, and to me it seems like non-government customers are also ready to scale tourism, media, research, and manufacturing in space.

Self-Funded Development: Most space companies require deep capital investment before they can begin to generate revenue. However, Axiom stands out from the pack because it can generate revenue as soon as it begins private missions to the ISS (while it is still developing its station) AND its ability to generate revenue scales each time it delivers a new module to the ISS. It may even be able to dictate its own pace of missions to the ISS once its modules are attached, which suggests even more early revenue growth potential. Additionally, given the publicity the station will be getting in/around 2024 with the launch of its planned production studio, brand partnerships could also represent early revenue upside. Management ultimately believes it can self-fund the majority of its station’s $3B construction costs, the rest offset by investor capital.

Other private space station developers may not have the benefit of conducting revenue-generating ISS missions before they build their stations, but all should be able to at least partially self-fund their station development via the process of build—>launch—>monetize and recoup costs—>repeat, with each subsequent module launched expanding revenue growth opportunities.

INVESTOR CONSIDERATIONS

Unless you are a VC, you can’t invest in Axiom, Nanoracks, or Blue Origin—they are all private companies.

SAD.

However, Axiom has hinted at going public to raise capital (and there are quite a few SPACs specifically targeting space that would probably love to take one of the 10 most valuable private space companies pubic), though I would anticipate Axiom waits until 2023/24 before doing so—that is the timeframe when the company’s capital requirements will be greatest + Axiom is launching its 1st module to the ISS in 2024, so there will be some natural media hype around the event.

Additionally, there are number of publicly traded companies you can invest in to get exposure to commercial space station construction.

Boeing ($BA) is assisting in the development of Axiom + Blue Origin’s space stations, and its Starliner crew vessel is expected to help transport both people and supplies to BO’s Orbital Reef down the road

Lockheed Martin ($LMT) is assisting with Nanorack’s Starlab space station

Maxar ($MAXR) is assisting with Axiom’s space station

Northrup Grumman ($NOC) is building one of the four stations being subsidized by NASA

Redwire ($RDW) is assisting with development of Blue Origin’s space station

Thales Alenia is assisting with development of Axiom’s space station—this company is owned by Thales Group ($THLLY) and Leonardo S.p.A.($FINMY)

(BRIEF) CONCLUSION

Regardless of whether the above companies are public or private, after doing this exercise I will be more closely watching the development of these commercial space stations, and I’m sure it won’t be hard to do so…media coverage of the subject is going pick up because:

There will be a production studio at the ISS…the media industry is sure to start caring more about space

Axiom’s 1st module launch in 2024 will be a historic moment and will certainly garner headlines

There will almost certainly be speculation that Axiom will go public via SPAC

That’s all for now, folks!