2022 Space Industry Key Themes - Part 3

Next-Gen Rockets

ESTIMATED READING TIME: 3 MIN (or just look at the pictures!)

This is the 3rd of a multi-part series previewing key themes for the space industry in 2022. Check out previous posts below:

Part 1: Geopolitical Competition (see here)

Past 2: Lunar Activity Ramping (see here)

There is a plethora of next-gen rockets attempting to reach orbit in 2022—up to six new heavy-lift rockets and nearly 40 new small/medium rockets across the globe!

This piece will focus on the six heavy-lift rockets + the top three upcoming private US small launchers that are all planning orbital launch attempts this year.

BFRs (BIG F*CK’N ROCKETS)

Governments and space agencies are eager to develop rockets that are bigger and more economical to launch at a high cadence relative to rockets in use now; these next-gen heavy-lift rockets will enable space infrastructure to be built in a more timely and cost-effective manner.

Obviously a bigger rocket enables for bigger payloads in a single mission, but additionally, the cost per kilogram to reach space generally improves the bigger the rocket being launched.

Each major space power is developing its own new heavy-lift rocket in order to maintain their autonomy in accessing space. Given the US’ burgeoning commercial space sector, it is not surprising to see that the country has the most new heavy-lift rockets in development (being pursued via both state and private workstreams); meanwhile Europe and China—which lag the US in terms of commercial space development (though China’s commercial sector is catching up)—are focused on 1-2 publicly-developed rockets each.

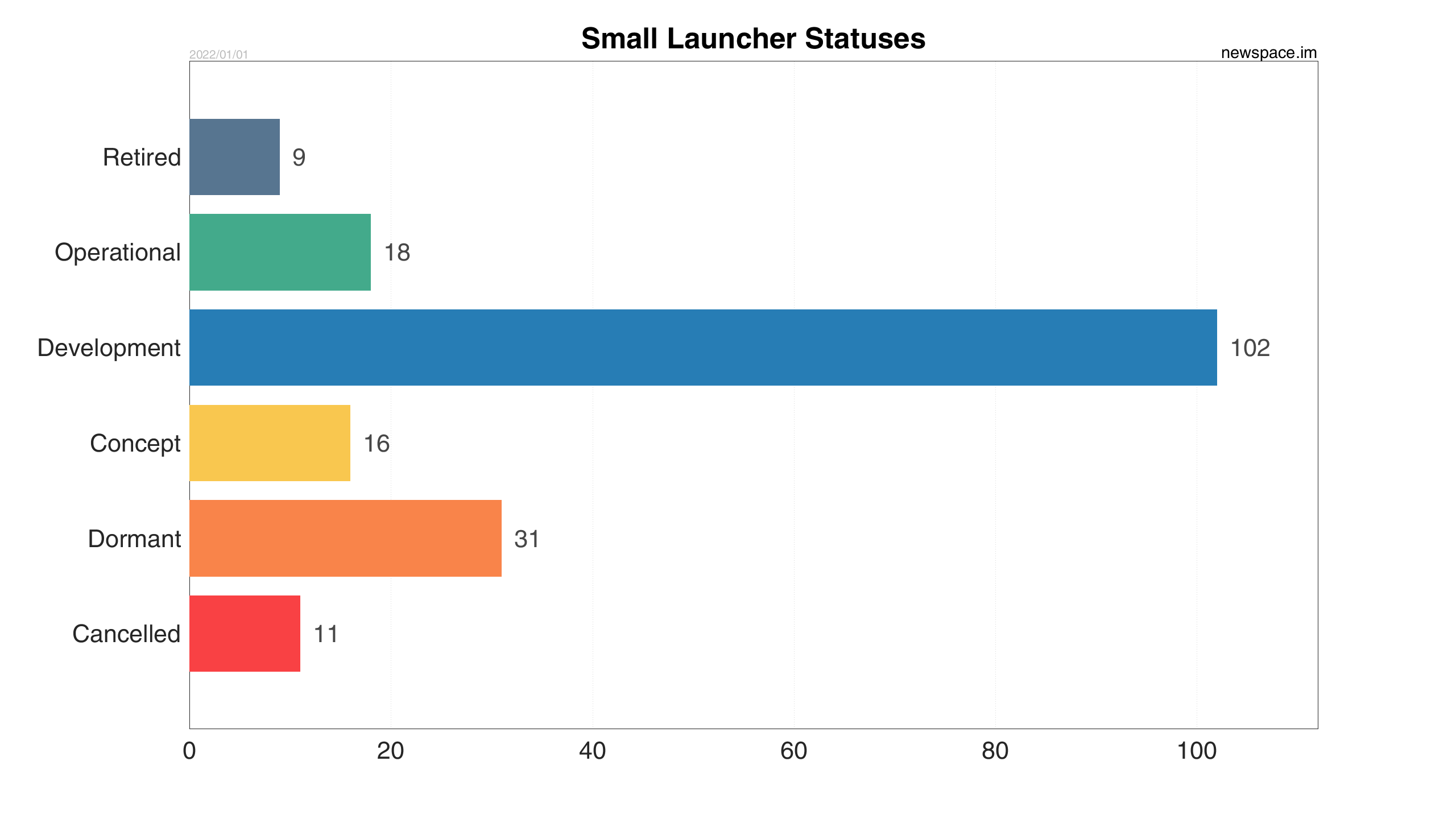

SMALL ROCKET PROLIFERATION

{kind=link}

There are nearly 40 small launchers aiming to reach orbit this year across the world—from the US to China, Argentina, Australia, Brazil, Canada, Germany, India, Japan, Romania, Singapore, South Korea, Sweden, and the UK.

The consensus opinion is that there will ultimately only be a handful of small launch winners given that most customers will choose larger rockets that offer better $/kg pricing vs small launchers, and there will be limited leftover demand for small rockets—I have to imagine most of these small rocket companies won’t survive the next five years, let alone ever reach profitability. However, it is likely that there will be a number of regional champions supported by local governments and A&D companies given that these groups will want to maintain autonomy + control their own access to space.

Recently, US pre-orbit launchers ABL Space Systems, Firefly Aerospace, and Relativity all have garnered >$1B valuations despite Rocket Lab, Astra, and Virgin Orbit’s head-starts in small-launch operations + SpaceX’s dominance outside of the small-launch category.

INVESTOR CONSIDERATIONS

So, why should investors care about the launchers mentioned even though the heavy-lifters are (mostly) not investable and the sentiment for small launchers is negative?

Heavy-Lift Rocket Read-Throughs

While it is unlikely that all six heavy-lift rockets make it to orbit (or even attempt to do so) in 2022, it is important to track their progress given that:

These rockets will offer the best unit economics for launch customers, and they therefore will set the baseline for pricing and competitive dynamics in the launch market; whatever demand they don’t satisfy will be leftover for small launchers

Most of these rockets are playing major roles in the progression of national space initiatives (including buildout of lunar infrastructure) and the construction of LEO satellite mega-constellations

Their failure or success could potentially influence space stock (or at least launcher stock) performance given that their launches will bring outside attention to the space industry

Small Launcher Read-Throughs

At first glance, a valuation comparison between the top private and public US small launchers doesn’t make sense; however, a closer look reveals some clear trends (see ‘Notes’ in the image above for individual company detail):

The highest value launchers are public/private market leaders that have aspirations to participate in lucrative cislunar/deep space activities.

The mid-tier launchers have gained traction with customers via their flexible launch offerings, but are primarily focused on the potentially limited small launch TAM.

The launchers with the lowest valuations have had progress overshadowed by bigger-picture issues.