I recently realized that I’ve spent about a year digging into “New Space” without stopping to really consider what the term means. Previously, I had a vague sense of what New Space is (e.g. SpaceX/other newer space companies = New Space and Boeing/Lockheed Martin/Northrup Grumman/other legacy aerospace & defense companies = Old Space), but if you had asked me to give a specific definition I’m not sure I would have had a real answer.

So in the spirit of year-end reflection, I stopped to formally investigate “what is New Space?”

During this exercise I learned about:

Old Space

NASA and US Space Policy

Cost-plus contracts vs fixed-price contracts

The rise of “new space companies” in the 2000s

The two biggest thematic unknowns facing space investors

My conclusion is that “New Space” both refers to:

Space activity where risks and costs are increasingly borne by the private sector rather than the public sector due to use of fixed-price contracting vs cost-plus contracting (a shift that primarily occurred in the early/mid-2000s).

Space companies founded in the 2000s that focus on lower-cost + rapid access to space and space technology, often utilizing iterative development methods.

**Note that I primarily focused on the US (as that is where I am from) and I am 29 (so I did my best with historical context).**

Old Space and Cost-Plus Contracting

Defining New Space starts with looking at “Old Space,” which I believe refers to space activity where risks and costs are borne by the public sector rather than by the private sector due to use of “cost-plus” contracting (i.e. most space activity up to the early/mid-2000s). Generally, legacy aerospace & defense (LA&D) companies are associated with Old Space; they are stereotyped as bureaucratic behemoths that have successfully helped the US achieve its space ambitions for decades, though in a slow and costly fashion. I would also argue that most space companies founded pre-2000s are Old Space as well.

In the past, access to space was primarily limited to nation-states and was almost entirely directed by government agencies that contracted aerospace & defense companies (using taxpayer dollars) to build the technology for a given mission. These agencies would award the aerospace & defense companies cost-plus contracts, which worked well in the early days of space exploration given unexpected and costly complications and delays that arose in the development of new space capabilities:

“The ‘cost-plus’ contract would include the total cost of making the system (satellite, launch vehicle or any smaller subsystem) plus a fixed-fee or a percentage that would count as “profit” for the company. It turned out to be a good deal for these companies and also made sure that the agencies had a direct say in the design of the spacecraft. Although, ‘cost-plus’ pricing was justifiable in the beginning as space companies faced stiff requirements and significant risk to build compliant, reliable, and performant systems, the inability to innovate fast enough and lack of competition in the market prompted the growth of NewSpace industry.”

The 2000s: A Transition Period for US Space Activity

There is a lot of history that I am going to gloss over between when the US reached the moon in 1969 and the early 2000s, but the overarching theme is that over time it became clear something needed to change—the cost to access space was astronomical and progress was too slow, resulting from a lack of competition amongst the Old Space companies that lobbied the government for space contracts.

In 2009, the Obama Administration instituted a review of the US’ human spaceflight plans and subsequent research confirmed that the current partnership model for space activity was indeed costly and slow: NASA estimated the average cost to launch the Space Shuttle was ~$450 million/mission (>$550M in 2021, accounting for inflation) and the US’ biggest human spaceflight program in progress at the time (the Constellation Program) was so behind schedule, underfunded, and over budget that the review committee determined that achieving any of the its goals wasn’t likely and it was scrapped.

This review (The Augustine Commission) ultimately led to a pivot in the US’ space policy in 2010: going forward, the US would look to increasingly rely on a broader scope of private companies to facilitate lower-cost access to space and space technologies, which would be accomplished by changing how NASA partnered with private companies and increasing competition in the commercial space sector. By lowering the cost of access to space and space tech, NASA’s budget could be more efficiently utilized to pursue research and exploration of space.

However, NASA had already begun to consider these objectives prior to 2010. In 2004 the Bush Administration had set forth a series of new goals for the US’ space exploration program (titled “Vision for Space Exploration”), and in 2006 as part of NASA’s strategic planning to achieve these exploration goals the agency announced an intent to explore new public-private partnership models that both supported NASA’s missions while at the same encouraging growth, competition, and technology breakthroughs within the commercial space sector. Changes included opening up bidding for launch service contracts to emerging US companies, as well as instituting prize competitions for demonstration of innovative space science or exploration technology.

Following the 2010 space policy pivot, NASA began to lean even more heavily into partnering with the commercial sector to achieve its goals + foster commercial market competition and innovation.

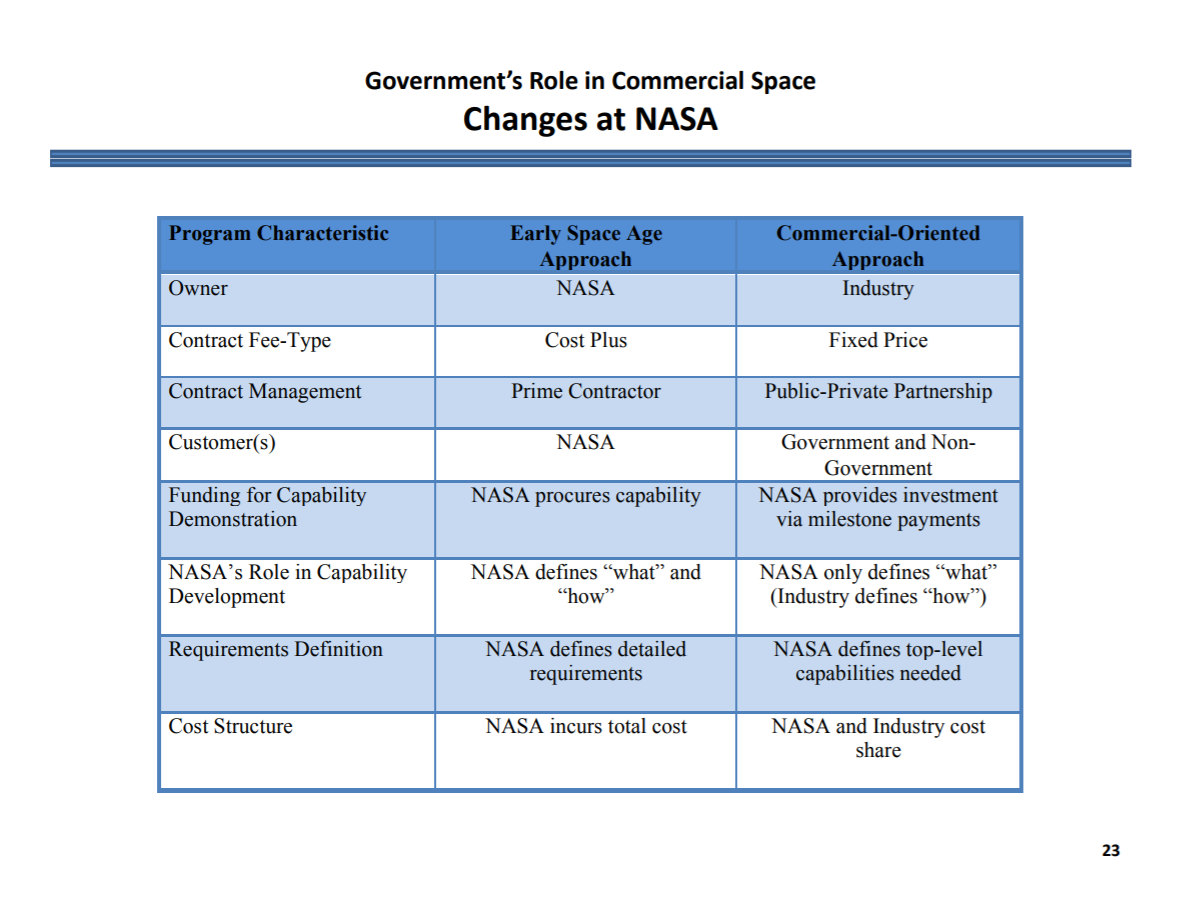

The following slides from NASA’s Ames Research Center (2015) summarize the changes in policy following the 2010 pivot + show how NASA’s new partnership model differed from the past (note that these slides are from 2015, a lot has changed since then obviously—they are meant to be illustrative):

Fixed-Price Contracts Fuel Innovation

One of the major differences with how NASA partnered with commercial companies post-2006/2010 was the introduction of fixed-price contracts vs the use of cost-plus contracts in the Old Space model. Given that the agency was looking to incentivize startups to meet its mission specs, NASA shifted to utilizing fixed-price contracts as a way to pay companies for meeting performance milestones rather than for making specific technology, therefore shifting the risk and cost of technology development to the private sector (i.e. NASA shifted from defining the “what” AND the “how” for its missions, to only defining “what,” leaving the “how” up to the contractor). This transition is best described by NASA, below:

“In contrast to cost-plus structures where most of the cost, schedule and outcome risks are borne by the government, fixed-cost procurement contracts shift many of the risks toward the contractor. With fixed-cost procurements, the contractor receives a pre-negotiated (i.e., fixed) value regardless of incurred expenses. Shifting cost responsibility to the contractor provides a positive profit incentive for cost and performance control, motivates the contractor to meet milestones, and allows for fair and reasonable price negotiation at the outset.”

- NASA, NASA.gov, “The Emerging Commercial Marketplace in Low-Earth Orbit”

As a result of this transition to fixed-price contracting / incentive-based compensation, a new wave of entrepreneurial space companies funded by private capital began to emerge in the mid-2000s. As a proxy for growth in the number of space startups, the chart below from BryceTech shows the number of space companies receiving outside investment—growth started in 2006 + accelerated in 2011, which matches the timeline for when NASA’s commercial partnership model began to change.

These “new space companies” focused on lower-cost and more rapid access to space to take advantage of the fixed-price contracts—the cheaper they could meet the specs required by a contract, the more profitable they could be, and the quicker a company could meet NASA performance milestones, the more contracts they could attempt to win.

This framework obviously required a different business development approach than was utilized during the Old Space era, and many of these newer companies utilize an iterative process to developing new technology with less capital and less time (SpaceX being a great example of a company using iterative tech development).

New Space Defined

So, bringing us back to the topic at hand (“What is New Space?”):

I believe New Space refers to space activity where risks and costs are increasingly borne by the private sector rather than the public sector due to use of fixed-price contracting. New Space companies have generally been founded in the 2000s and focus on lower-cost + rapid access to space and space technology via iterative development methods.

While both New and Old Space companies partner with governments, most New Space companies have the goal of eventually NOT being entirely dependent upon government contracts the way that many Old Space companies are—government demand is undoubtedly a key driver of early growth for any new space company, but most New Space companies point to an expectation for increasing non-government demand over time (look at any New Space SPAC investor presentation if you need evidence), which has attracted considerable institutional investor funding (from VC to PE to public equity investors).

Additionally, the emergence of New Space hasn’t killed Old Space—in fact, the distinction between Old Space and New Space has started to blur. Old Space companies have acquired New Space companies (most recently Aerojet Rocketdyne was acquired by Lockheed Martin), partnered amongst themselves (Boeing and Lockheed partnering in 2006 to create the United Launch Alliance JV is the most notable example here), and they have even invested in some New Space companies (Lockheed was an early investor in Rocket Lab).

Space Economy TAM: The Biggest Thematic Unknown

Okay so in the context of what I’ve gone through so far, and given that New Space companies are becoming a more prominent sector of investment for both private and public capital, I believe biggest thematic questions for space investors and companies are:

How large will government investment in the commercial sector be?

How large will non-government demand really be, and over what time period will it reach forecasted levels?

I will not pontificate on answers to either of these questions now—that discussion could make for its own bajillion word post.

However, current forecasts for the space economy in total suggest there is material growth ahead for the industry in the coming decades—Wall Street estimates that the space economy could grow from ~$350M in 2016, to >$1T by 2040 (some forecasts going as high ~$3T by 2040 or 2045).

But skeptics have rightfully questioned these astronomical projections:

For example, the federally funded Science and Technology Policy Institute notes that the aforementioned estimates from financial institutions for both the current size of the space economy as well as projections for future growth use flawed methodology (see reasoning below).

Optimism vs Reality

New Space companies obviously have at their core an optimistic ethos—they are pushing the forefront of technology being used to explore the “final frontier.” And New Space founders are obviously not going to dispute forecasts for industry growth that paint a positive picture regardless of what they actually believe to be true, given growing investor enthusiasm for investing in space—they are (and should be) taking advantage of easy access to capital while it is readily available, and while analysts are painting a rosy picture of industry tailwinds (before the future becomes reality, and the narrative potentially changes).

It is therefore imperative that investors carefully consider which New Space management teams are most trustworthy when making investment decisions.

For public equity investors, performance YTD in 2021 (solid double-digit negative returns for all but Rocket Lab) suggests that investors may be skeptical of the growth projections laid out by many of the New Space companies. Near-term share price appreciation for public space companies will come down to performance relative to communicated guidance—I’m looking forward 4Q21 earnings calls and seeing how management teams communicate their outlooks for 2022.