To the Moon? Reviewing the Intuitive Machines SPAC Deal

Intuitive Machines (future ticker LUNR) is the only SPAC that can actually take investors to the moon—but does that mean you should invest in the stock?

I spent this past weekend reviewing the Intuitive Machines SPAC investor presentation (link), and the company clearly wants to take over the moon.

Not in the literal sense (duh), but its SPAC deal announcement is a signal that Intuitive Machines is attempting to dominate the lunar economy.

There is a lot of info in the SPAC deck—to help us separate the signal from the noise, in this post I will narrow our focus to:

Strategic Rationale

Projected Financials

Valuation

After reviewing those three areas of the presentation, I will share my own opinion of the deal in the “conclusion” section of this post.

Note: if you aren’t familiar with Intuitive Machines, see this article from the Wall Street Journal for some context (link).

STRATEGIC RATIONALE

Why Now? What is the Opportunity?

Intuitive Machines is looking to capitalize upon its success to-date.

The company has received three Commercial Lunar Payload Services (CLPS) awards from NASA—more than any other competitor—to deliver scientific instruments and equipment to the Moon to gather data in preparation for human exploration later in the 2020s.

Management thinks NOW is the time to accelerate the company’s business plans because of the shifting battlefield of geopolitical competition.

They believe the US federal government plans to use lunar exploration to project soft power and 'maintain the high ground' vs China and Russia.

Unlike in the past, NASA and the US government will heavily rely on public-private partnerships to accomplish their goals in this 21st century space race.

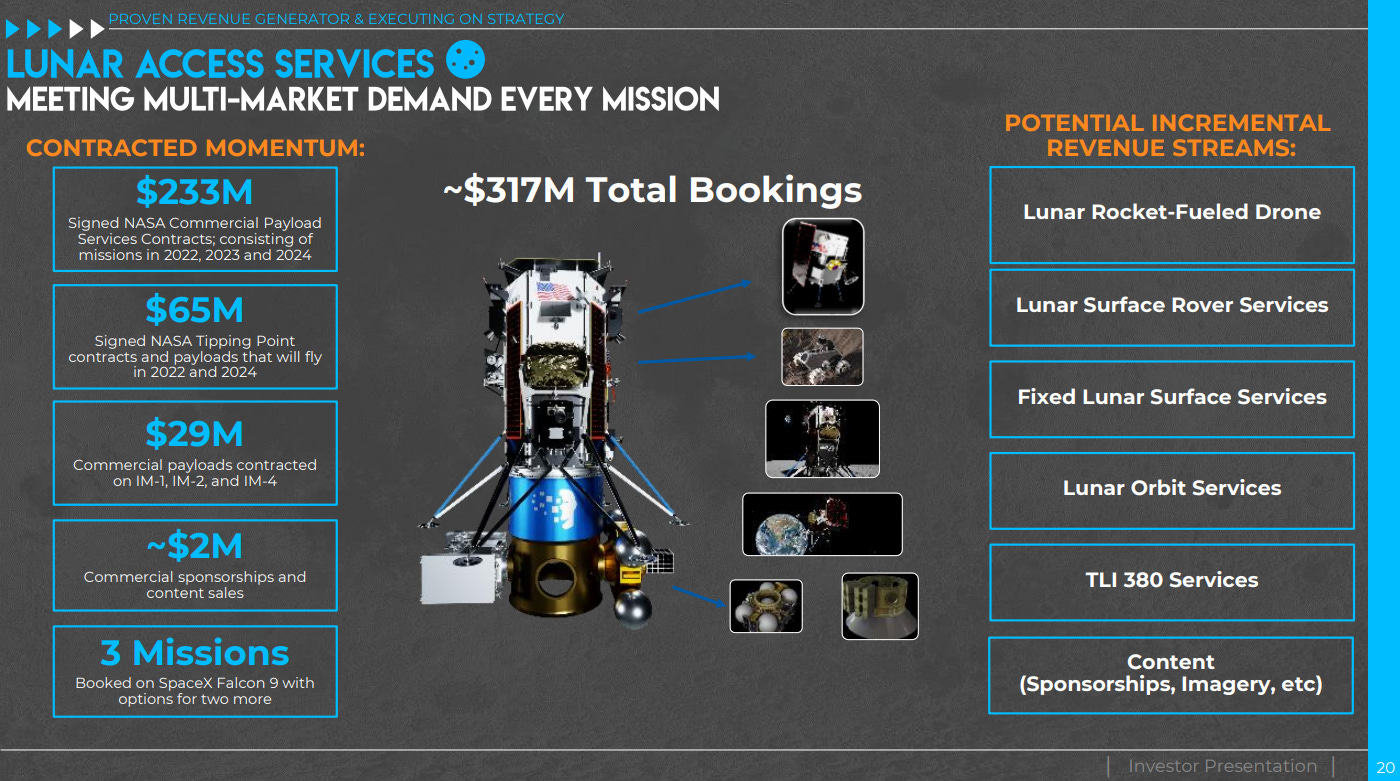

There is upwards of $90B earmarked for lunar exploration missions through the late 2020s, and LUNR has already secured ~$300M worth of contracts from this federal lunar mission funding.

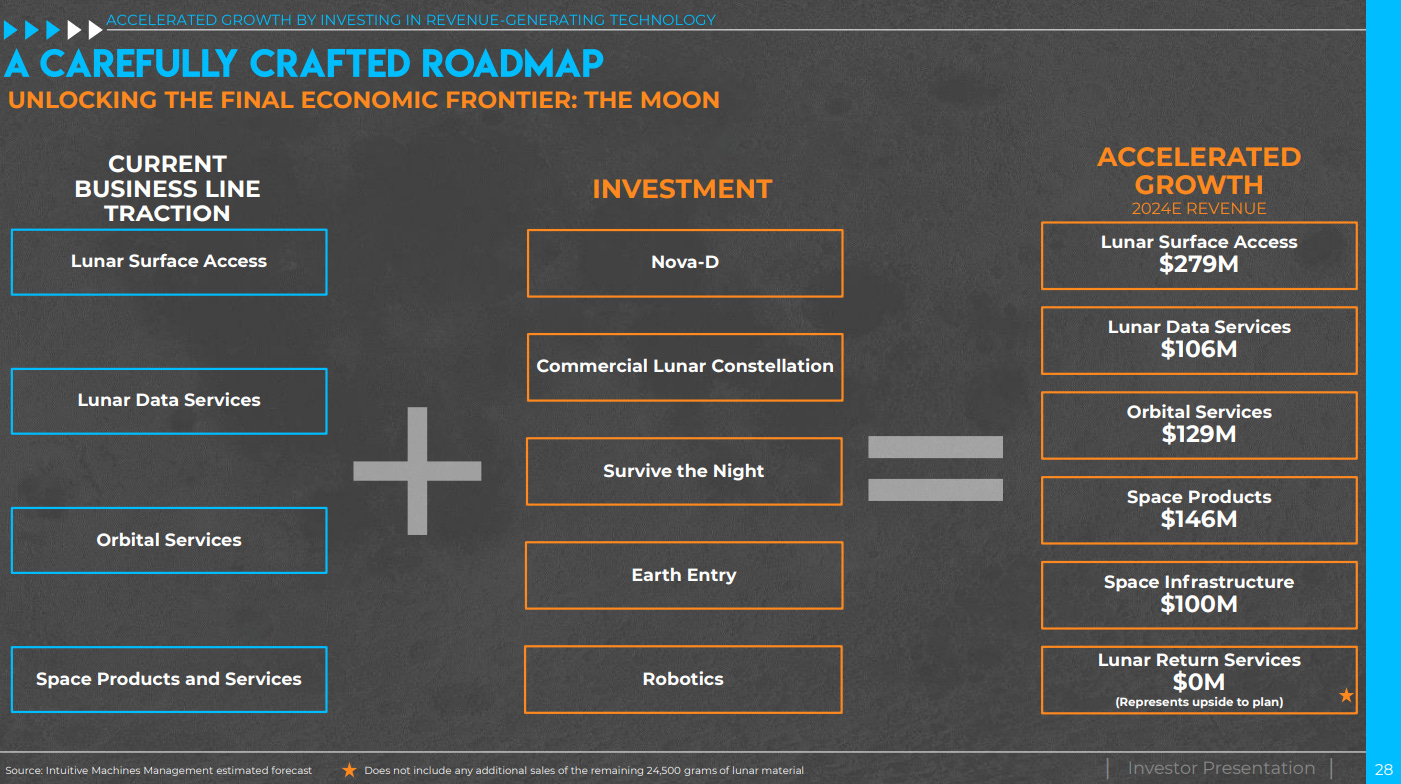

By raising up to $331M in capital by going public via SPAC, management hopes to outpace competition by investing to develop new technology that can help the company capture an even larger share of the lunar economy, as it develops over the next decade.

Additionally, Intuitive Machines plans to further monetize the technology and space systems it is developing for its lunar access program by providing orbital services, space products and infrastructure, and specialized aerospace engineering services for 3rd party missions.

However, management is clearly primarily focused on the lunar opportunity based on how they present the total addressable market.

FINANCIAL PROJECTIONS

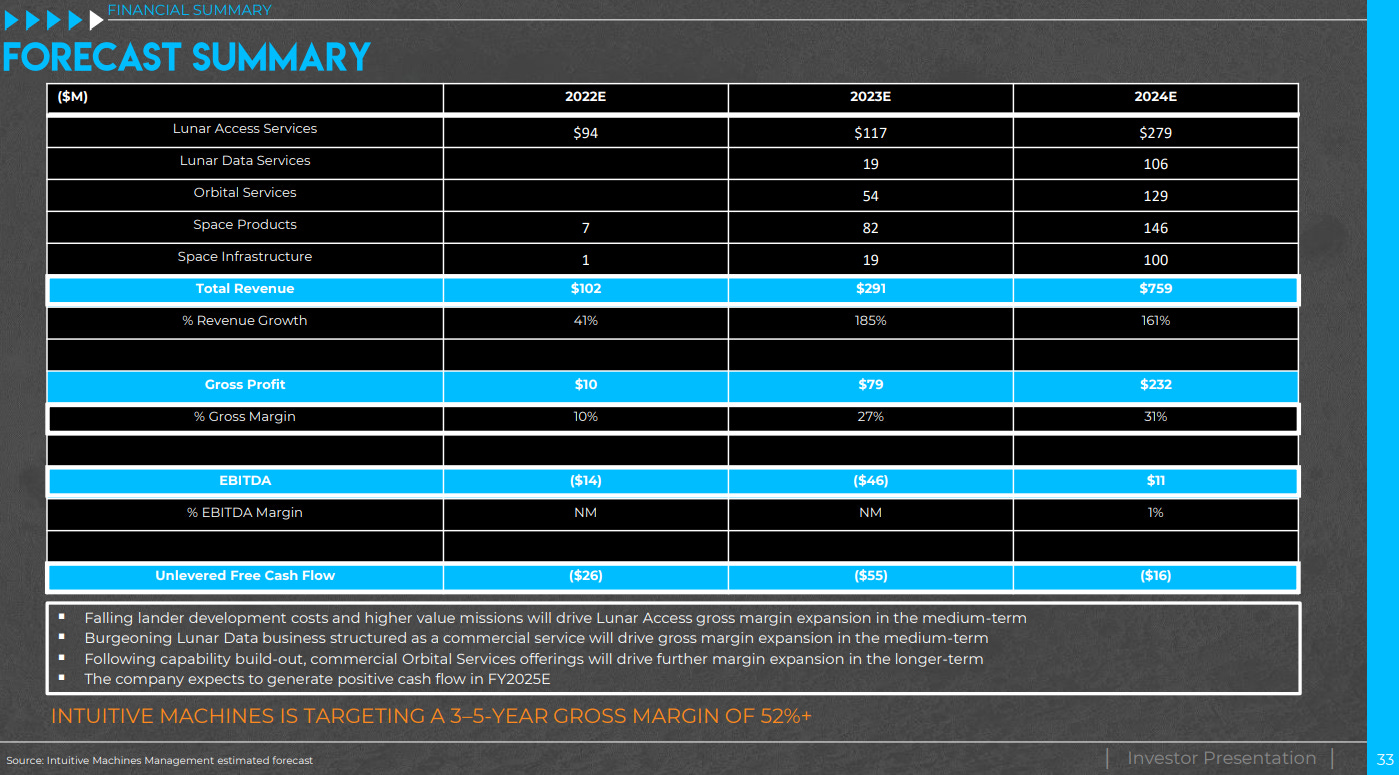

REVENUE

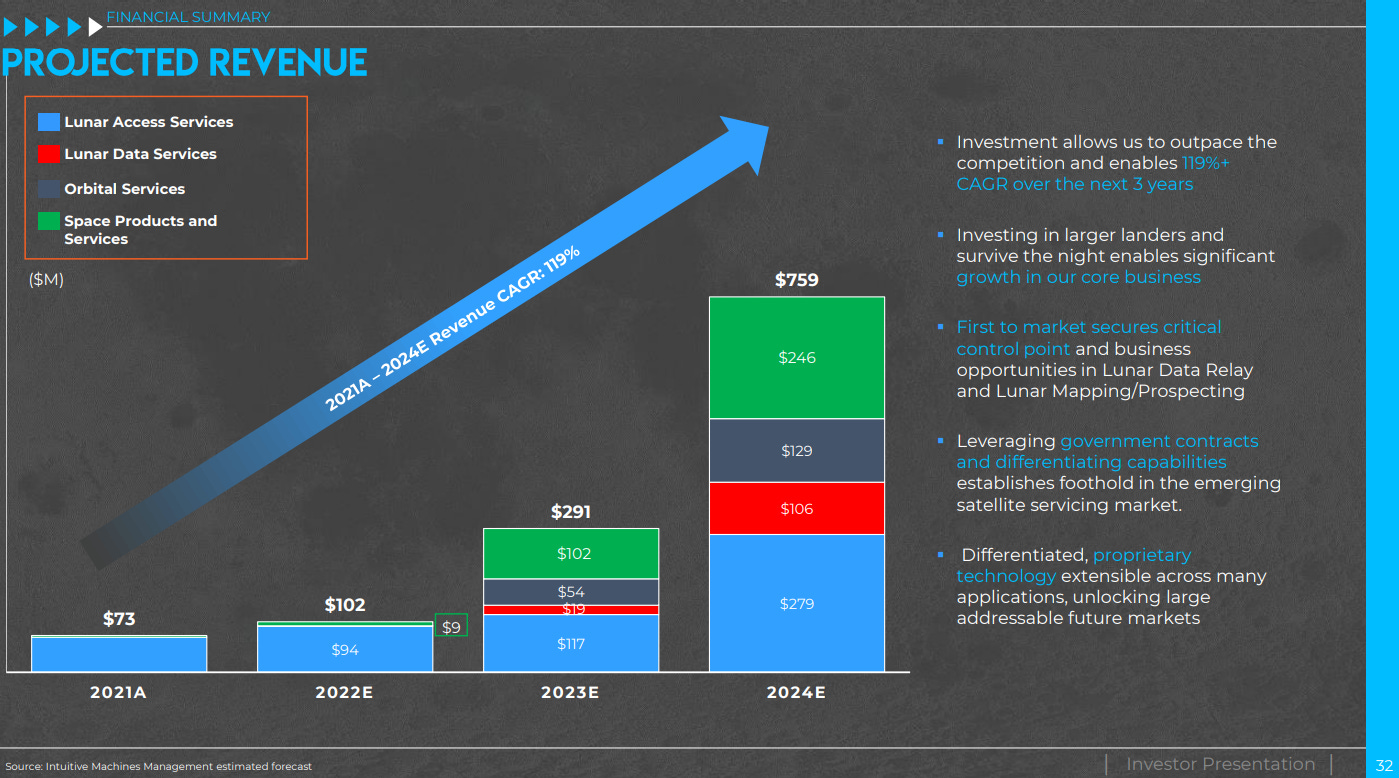

To date, Intuitive Machines has really only generated revenue via Lunar Access Services, aka via steady funding from NASA's CLPS program.

However, LUNR hopes to grow total revenue 7.5x from 2022 to 2024 by diversifying its revenue streams into 3 new lines of business (detail in the 2nd image below), going from 91% of revenue coming from Lunar Access Services in 2022 to only 37% from Lunar Access Services in 2024.

In the meantime, Lunar Access Services will grow >3x from 2022 to 2024.

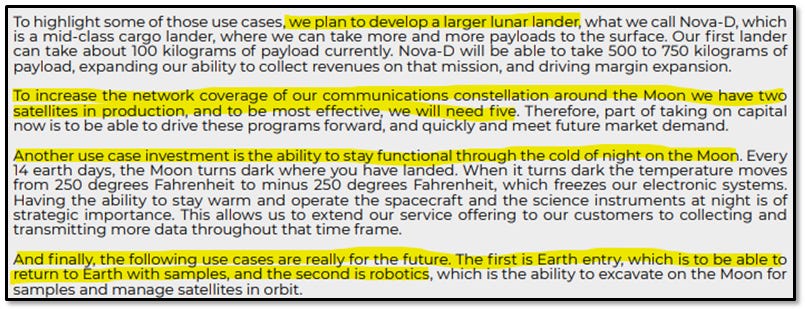

This growth will be driven by development of a larger lander, ability to survive the lunar night and increased mission frequency + complexity.

Intuitive Machines’ three other planned types of revenue are projected to have astounding growth, going from just $9M in 2022 (9% of total revenue) to $481M in 2024 (63% of total revenue).

Given that most of LUNR’s revenue is coming from government contracts, management has a high degree of confidence in its 2022 and 2023 financial outlook—100% of 2022 revenue is already contracted and 53% of 2023 revenue is already contracted.

MARGINS AND PROFITABILITY

Looking at margins, it makes sense why Intuitive Machines is looking to invest in new technologies to scale its Lunar Access Services and diversify its revenue streams.

While Lunar Access Services is gross margin positive, 10% GM won’t cut it long-term. As LUNR’s other higher-margin revenue streams scale through 2024, they will drive gross margin expansion to 52% long-term, and EBITDA and Free Cash Flow will break even by 2024 and 2025, respectively.

VALUATION

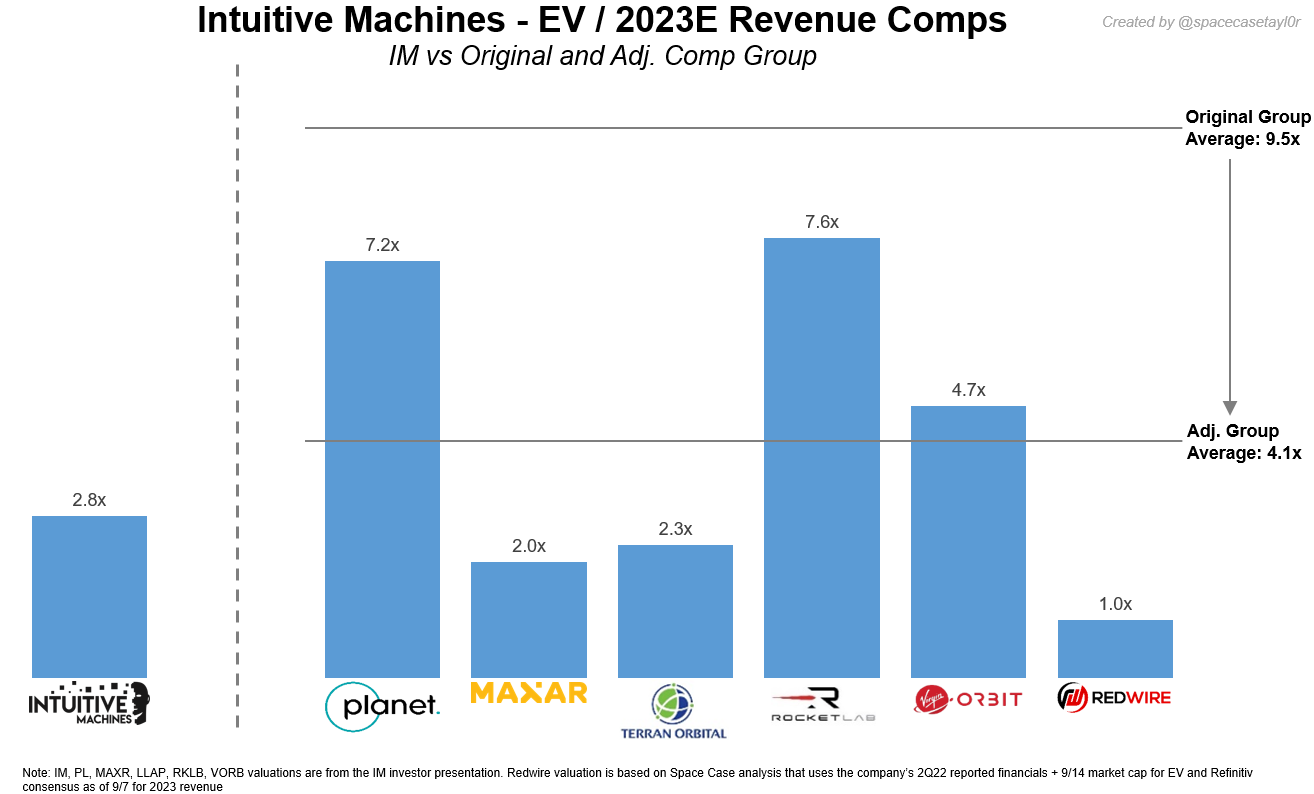

At first glance, LUNR’s 2.8x Enterprise Value / 2023 Revenue multiple looks cheap vs its comparable group average multiple of 9.5x.

When choosing the group of companies to compare LUNR against, I assume the bankers were focusing on space pure-plays that have, or are developing, extensive in-house manufacturing capabilities.

If this is the case, a curious omission from the group was Redwire Space, which is heavily involved in space systems manufacturing, government contracting, and space exploration missions.

Additionally, I am not a fan of including Virgin Galactic. If Intuitive Machines is being valued on 2023 revenue, then it makes sense to include companies forecasted to generate material revenue in 2023 in this comparison—Virgin Galactic is forecasted to generated just $24M of revenue in 2023 vs every other company in this comparison is forecasted to generated at least $250M of revenue in 2023.

If we exclude Virgin Galactic and include Redwire Space, LUNR’s 2.8x now compares to a 4.1x group average.

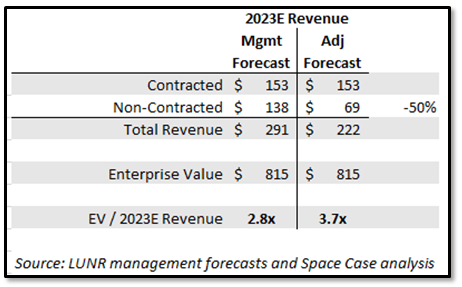

Additionally, we can’t just take management’s revenue forecast for granted—too often we have seen the space SPACs (and SPACs in general) lower guidance immediately following their deal close.

LUNR gets some benefit of the doubt since they have contracted 53% of their forecasted $291M 2023 revenue—but what does their valuation look like if they only capture 1/2 of the $138M of uncontracted, forecasted revenue?

LUNR’s multiple would increase to 3.7x, which is still favorable vs the comparable group average multiple of 4.1x, but significantly less so than vs the 9.5x shown in Intuitive Machine’s presentation.

CONCLUSION

LUNR management paints a grand picture of their company acting as a key player in the development of the lunar economy and the 21st space race drama set to unfold in the coming years, and their arguments for “why now” and “what is the opportunity” are compelling…

HOWEVER **record scratches**

…a huge portion of their financial outlook relies upon securing substantial Orbital Services and Space Products + Services revenue in 2023 and 2024.

Going from $9M of these two revenue streams in 2022 to $375M in 2024 is a classic “hockey stick” forecast—something we have learned to be skeptical of in SPAC presentations.

Scaling on-orbit + manufacturing businesses take time—ask Momentus, Rocket Labs, Virgin Orbit, Terran Orbital, Redwire, etc, which are all in the multi-year process of scaling their space systems and manufacturing operations, including hiring, building the facilities, and acquiring new business.

This is an increasingly competitive area within the space industry, and I will wait for evidence that LUNR is seeing traction in the market before I buy their story that they can scale this higher-margin revenue that is the key to their EBITDA and FCF breakeven forecasts by 2024/25.

I am more optimistic about the outlook for LUNR’s Lunar Access Services revenue. This is currently a low-margin revenue stream given that Intuitive Machines is partly winning contracts by acting as a low-cost provider for NASA, but investments in a larger lander, ability to survive the lunar night, and increased mission frequency and complexity should all drive more revenue (both per mission and overall) and therefore higher margins. However, I expect the timescale required for this revenue stream to become a more meaningful margin contributor is several years off—hopefully management can provide more detail about the timeline for these technology developments at their investor day before de-SPACing.

Lastly, I am uncertain how much of Intuitive Machines’ business plan can be achieved if there are material SPAC redemptions that drive down the amount of capital this deal raises (the max amount the deal can raise is $331M, but we have recently been seeing significant reductions in SPAC deal sizes due to high redemption rates). There is only $55M of committed capital from SPAC sponsors, and the SPAC sponsors originally set out to focus on “consumer-facing” technology—closing on a government-contracting space business is…surprising. Are they really in this business for the long-haul?

Overall, I absolutely agree with the Intuitive Machines management team’s decision to “capitalize on momentum to outpace the competition,” but I am skeptical of management’s forecast for growth of higher-margin non-Lunar Access Services revenue and am wary that the deal may not ultimately raise enough capital to fund the company’s next-gen lunar access technology. I expect LUNR will be a volatile stock driven by contract wins/losses and successful/unsuccessful lunar missions. Though deal valuation wasn’t horrible, I would be more tempted to buy-in to the stock below current pricing.

Very comprehensive analysis. IM looks to be on track of Hockey Stick growth based on recent developments. What are your thoughts?