February 2025 Space Stock Review

Includes Commentary on ASTS, RKLB, RDW, LUNR, PL, SPIR, SESG, and ETL

Hello fellow space enthusiasts! 🚀

In this month’s Space Stock Review:

📈 Market Overview

✍️ Space Stock Performance + Valuation

RKLB, PL, RDW, and LUNR vibe checked

SPIR + Kpler go to court

Starlink Super Bowl ad boosts ASTS + $43M SDA deal

Boardroom drama spoils ETL.PA earnings

Potential C-band sales drive SESG.PA

Disclosure/Disclaimer: Case Closed should not be interpreted as investment advice or an investment recommendation; posts represent Case’s personal opinions only. Please do your own research before investing.

1. MARKET COMMENTARY

Public Markets

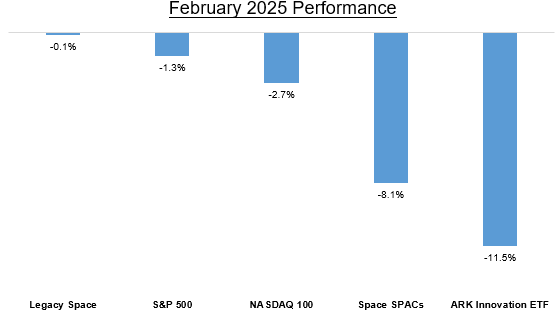

The markets experienced a vibe shift in February 2025, as increasingly glaring risks ranging from economic slowdown to geopolitics, trade wars, and lofty valuations resulted in heightened stock volatility; riskier assets like the space SPACs and companies held by the ARK Innovation ETF experienced a sharp correction in February, erasing gains made in January.

Notably, while macro uncertainty is already at extreme levels, market uncertainty is still rising (see charts below). Given that it seems unlikely economic and geopolitical uncertainty will be resolved in the near-term, I think there’s room for fear in the markets to increase, and investors should probably buckle up for continued volatility

Private Markets

I won’t go into as much private market detail here, but check out these resources for private market news and/or trends:

Karman Space & Defense’s IPO Raises $506 Million, Priced Above Range

Note from Space Case: We plan to add Karman Space & Defense (KRMN) to our space stock tracker in future editions of Case Closed—stay tuned!

Historical returns for name-brand VCs:

2. SPACE STOCK COMMENTARY

Rocket Lab / RKLB (-29%), Planet Labs / PL (-24%), Redwire / RDW (-42%), and Intuitive Machines / LUNR (-33%) all saw January gains wiped out in February, though they remain well above their pre-election levels

I am not surprised to see these four stocks decline in February given that they had gone up +163% after the T2 Admin’s US election win in early November through the end of January

While material post-election news like Planet Labs’ $230M deal to manufacture satellites for SKY Perfect JSAT or Redwire’s acquisition of Edge Autonomy might have actually justified such large stock movement, I think it makes sense that these four stocks pulled back in February amid the market’s negative vibe shift in February given their outsized gains since November

Spire Global / SPIR declined -33% in February after the company disclosed that it was suing Belgian analytics provider Kpler for backing out of a deal to acquire SPIR’s commercial ship-tracking business for $241M (link to SEC filing)

Spire Global announced plans to sell its maritime business in November 2024, with anticipated deal close in early 2025. Despite Spire claiming the deal process met all conditions for closing up to this point, Kpler refused to close the deal, leading Spire to sue for enforcement and breach of contract with the Delaware Chancery Court on 2/10

Investors reacted poorly to this news, with SPIR shares declining -49% the day after Spire disclosed the lawsuit. Spire had intended to use the proceeds from this transaction to eliminate its outstanding debt and invest in growth opportunities; without the cash infusion from this asset sale, Spire faces near-term debt repayment challenges (>$90M due for repayment within 12mo from 3Q24). Investors are clearly concerned about the company’s ability to manage its debt obligations given that Spire only had $19.2M of cash on hand as of 12/31/2024 (link)

AST SpaceMobile / ASTS went up +34% in February as Direct-to-Cell (D2C) satellite communications (satcom) went mainstream and the company disclosed its 1st firm revenue-generating contract

On 2/9, T-Mobile / TMUS aired a Super Bowl commercial announcing the beta launch of its D2C service in partnership with Starlink (link to video). While this commercial didn’t directly involve AST SpaceMobile, ASTS shares increased +17% the next day because the commercial 1) brought attention to the growing interest in D2C and with AST being the only publicly traded D2C pure play, it likely benefitted from the related Starlink x T-Mobile media buzz; and 2) the Starlink x T-Mobile D2C service’s pricing & packaging (free for T-Mobile’s premium tier service customer, $15/mo for other T-Mobile customers, and $20/mo for non-T-Mobile customers) revealed key details that investors have debated for some time. In particular, the $15-$20/mo pricing was significantly higher than most had anticipated for consumer D2C service, and given that this was for Starlink’s text-only level of connectivity (for now), AST shareholders viewed this news as a positive sign of a “floor” pricing for D2C (at least in the US) since AST’s D2C service is expected to provide broadband-level data rates

However, I believe T-Mobile’s pricing & packaging structure is set up to drive customers to the company’s premium service tier (Go5G Next, $100/mo for 1 line), and in general I believe this will be the primary motivation for how US wireless carriers structure D2C pricing & packaging; I think it is unlikely that many customers will pay $15-$20/mo specifically for D2C service more often than when they know they will need it (such as when they have planned travel to remote areas that are known to be out of traditional cellular network range)

If we go along with my assumption that consumer D2C service usage will primarily come from customers who get it for “free” via their premium tier wireless data plans, then revenue kickback to D2C providers will be based on actual D2C usage, akin to how roaming fees are charged to a customer’s account when they use their mobile devices outside their provider's coverage area, incurring charges based on the services consumed on a partner network. In this light, instead of assuming D2C operators get 50% of $15-$20/mo, they will get 50% of something more along the lines of roaming fees; for reference, T-Mobile’s current roaming fee structure is $0.10/text, $0.25/min for calls, and $2-$5/MB of data (link)

On 2/26, AST announced it had won $43M from a prime contractor in support of the US Space Development Agency’s (SDA) Proliferated Warfighter Space Architecture (PWSA); the SDA is a U.S. Department of Defense agency focused on deploying a resilient, low Earth orbit satellite network (the PWSA) for military communications, missile tracking, and data transport. While ASTS had technically previously signed revenue-generating contracts with AT&T (based on technology readiness) and Vodafone (minimum revenue commitment), I view this SDA contract as the company’s 1st firm, multi-million dollar contract. Of note, the language in the company’s press release for this SDA contract (link) makes it clear that the $43M is not related to AST’s participation in the SDA’s HALO program, where the company has the opportunity to compete directly as a prime contractor for specific prototype orders (link).

In general, I think the D2C market for government customers is more compelling than the opportunity for consumer customers, and I view AST’s quicker go-to-market success with government customers as proof of this. Government agencies, especially the military and emergency responders, require reliable communication in remote areas where terrestrial coverage is absent; while legacy fixed or mobile satcom services can solve this problem by providing connectivity in areas where terrestrial networks can’t, they require specific user hardware that is oftentimes bulky and/or very expensive. Consumers may view 100% network availability as a “nice to have,” but government customers cannot afford service lapses. They already view legacy satcom-enabled connectivity as mission-critical (hence tens of billions of dollars per year in dedicated budget for satcom) and I think the potential for D2C mobile connectivity via “ruggedized” standard devices has the potential to unlock enhanced satcom capabilities relative to legacy solutions

Eutelsat / ETL.PA saw shares decrease -31% in February following an unusual earnings announcement

Eutelsat reported fiscal 1H25 results on 2/14 and although results were in-line with expectations (with OneWeb monetization continuing to disappoint), the big news of the day was that four members of the company’s board of directors announced their resignation and the chairman of the board announced their retirement (link)! Although the press release uses the words “resign” and “retire” I can’t help but wonder about this highly unusual event. Eutelsat shares were down -19% the day of the earnings release, and they continued to decline throughout the rest of February

SES / SESG.PA saw shares increase +34% in February following speculation around returns from C-band spectrum sales and strong 4Q earnings relative vs guidance

On 2/6 the FCC announced that it was considering changing how the upper portion of C-band spectrum is used (link); the spectrum in question is currently owned by geostationary (GEO) satellite operators SES and Eutelsat. In the past, a different portion of C-band spectrum (owned by Intelsat (soon to be acquired by SES), SES, and Eutelsat) was auctioned off by the FCC so that wireless companies (mostly Verizon, AT&T, and T-Mobile) could use it for 5G; the satellite owners were given a portion of auction proceeds ($9.7B) as compensation. SESG.PA shares increased +11% the day after this news broke, and shares continued to increase for a week+ afterwards; one analyst estimated that SES could see over $2.9B in proceeds if this C-band spectrum was auctioned off at similar pricing as the prior C-band auction (link)

On 2/26, SES posted 4Q24 earnings, which beat management’s previously issued guidance, with strength in the company’s Government (U.S. and international) and Mobility (aviation and cruise) segments. Of note, on the earnings call management 1) highlighted the new C-band spectrum sale potential, noting that the T2 Admin’s FCC is motivated to move quickly to generate revenue for the US Treasury (via spectrum sales); and 2) reaffirmed SES’s plans to close its proposed merger with Intelsat in 2H25 and noted that original guidance for the newco’s financial profile is unchanged. These details were viewed positively in contrast to Moody’s downgrade of SES’ outlook from stable to negative on 2/18 (link)

Is this series going to continue? Hope so! 🍀